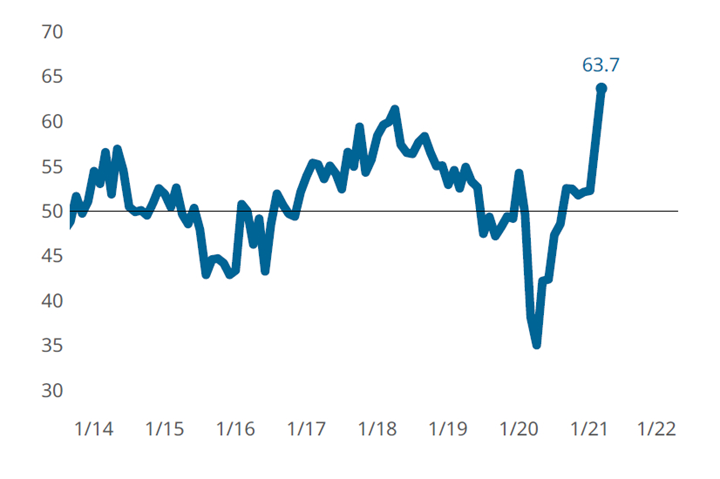

Composites Index jumps five points to an all-time high

Volatile March survey finds troubled supply chains and strong demand.

.jpg;width=70;height=70;mode=crop;format=webp)

Share

Read Next

The Composites Fabricating Index set a new all-time high due to elevated supplier delivery, new orders and production readings.

The GBI: Composites Fabricating Index rose more than five points in March to close at a new all-time high of 63.7. The month’s gains were broad-based. Supplier delivery, new orders, production and backlog activity all reported quickening expansion. Slowing the Index’s ascent were employment activity, which registered decelerating growth, and a contraction in export activity.

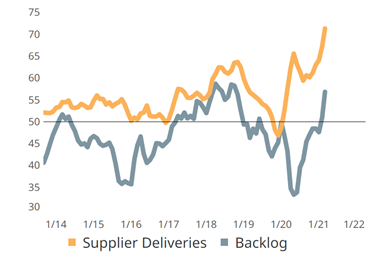

Supply chain difficulties are restricting production which, in the face of strong demand, has caused a meteoric rise in backlog activity.

New orders and production readings maintained a nearly five-point spread which was first observed in February. During the fourth quarter of 2020 through January, fabricators reported modestly contracting backlog activity. Since that time through March, however, backlog readings have quickly expanded, resulting in this month’s all-time high backlog reading. Much of this volatility is attributed to crippled supply chains and strong demand. The current supplier delivery reading in excess of 78 is roughly 13 points higher than the pre-COVID-19 peak reading of nearly 65. However, this 13-point spread represents as much as a 90% increase in the number of survey respondents who reported worsening supply chain conditions as compared to the prior peak.

Related Content

-

Composites industry gained back some ground in December

The GBI: Composites Fabricating contracted a little more slowly in December, landing between August and September 2023 values.

-

Composites GBI remains relatively unchanged in May

The GBI: Composites closed May at the same reading reported in April, with some minor fluctuations in component activity.

-

Composites industry index was flat for March

The GBI: Composites Fabricating closed March flat, losing 1.3 of the 3.1 points gained in February.