Composites Business Index 50.2: Industry flat since July

Gardner Business Media's (Cincinnati, Ohio) director of market intelligence Steve Kline, Jr., reviews the Composites Business Index for August and September 2014.

.JPG;width=70;height=70;mode=crop;format=webp)

Steve Kline is the director of market intelligence for Gardner Business Media Inc. (Cincinnati, Ohio), the parent company and publisher of High-Performance Composites. Kline holds a BS in civil engineering from Vanderbilt University and an MBA from the University of Cincinnati.

The Composites Business Index for August and September 2014.

Share

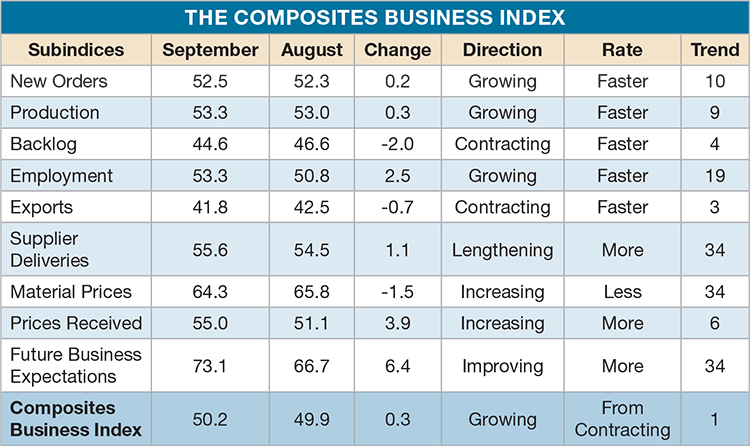

In August, our Composites Business Index (CBI) read 49.9, indicating the industry was essentially flat after 10 consecutive months of growth. Nonetheless, the Index was higher than it was one year earlier. In fact, the month-over-month rate of change had grown since September 2013, and the annual rate of change had accelerated for seven months.

Also, there were some positives in the subindices. New orders increased for the ninth month in a row, and production expanded for the eighth straight month. Although backlogs contracted for a third month, the rate was slower and its index was 17.4 percent higher than one year earlier and had shown accelerated growth every month in 2014 — a very strong sign that capacity utilization and capital equipment investment will grow through 2015. Employment grew, but at its slowest rate since June 2013. Exports had contracted sharply for two months, falling to their lowest level since the index began (December 2011). Supplier deliveries had lengthened at a moderately increasing rate since October 2013.

Material prices continued to increase, near peak levels reached since January 2012. Prices received were up for the fifth straight month — the longest stretch of increases since summer 2012. Future business expectations were at their lowest level since September 2013.

Mid-size facilities (20 to 249 employees) continued to expand. Those with less than 19 employees had contracted four of the previous six months. Facilities with more than 250 employees contracted for the first time since October 2013.

Regionally the West and Northeast, expanded. The North Central – West contracted after expanding in July. Both the North Central – East and the Southeast had contracted for two straight months.

Future capital spending plans contracted for a second month. The annual rate of growth slid to its second slowest rate since November 2013.

September’s CBI of 50.2 indicated a slight overall expansion, but the industry remained flat for a fourth month. The rate of change was a mere 2.4 percent, the slowest month-over-month growth since August 2013. For the first time in 2014, the annual rate of growth decelerated.

New orders grew for the tenth consecutive month, at a rate virtually unchanged for three months. Production expanded for a ninth month. The rate of expansion, had slowed since June, but ticked up slightly. Backlogs contracted for a fourth month, but its index was 2.5 percent higher than one year earlier. Significant growth in the annual rate of change was another strong sign that capacity utilization and capital equipment investment will increase through 2015. Employment growth accelerated noticeably compared to the previous two months. For a second month, exports contracted at their fastest rate in CBI history. Supplier deliveries lengthened again, and had done so at an accelerating rate since June.

Material prices continued to increase, but growth had slowed since May and September saw the slowest rate of 2014. Prices received had increased for six straight months — their longest sustained stretch since summer 2012. Prices received were at their highest since June 2012. After falling significantly for two months, future business expectations rebounded sharply.

Larger facilities continued to see exceptional growth at an accelerating rate. Mid-size plants contracted for the first time since December 2013, and the rate was the fastest since December 2012. Plants with less than 20 employees contracted for the third month in a row.

For a second month, only two regions expanded. The West was the best performer again. The only other region to grow was the Southeast, for the first time since May. Contraction was relatively moderate in the Northeast, and North Central – East accelerated as it had during the two preceding months.

Future capital spending plans contracted for a third month, but the rate had slowed each month. Although the annual rate of change went up, it did so at its slowest rate in the past year.

.jpg;maxWidth=300;quality=90;format=webp)

Read Next

All-recycled, needle-punched nonwoven CFRP slashes carbon footprint of Formula 2 seat

Dallara and Tenowo collaborate to produce a race-ready Formula 2 seat using recycled carbon fiber, reducing CO2 emissions by 97.5% compared to virgin materials.

Read More

“Structured air” TPS safeguards composite structures

Powered by an 85% air/15% pure polyimide aerogel, Blueshift’s novel material system protects structures during transient thermal events from -200°C to beyond 2400°C for rockets, battery boxes and more.

Read More

Plant tour: Daher Shap’in TechCenter and composites production plant, Saint-Aignan-de-Grandlieu, France

Co-located R&D and production advance OOA thermosets, thermoplastics, welding, recycling and digital technologies for faster processing and certification of lighter, more sustainable composites.

Read More