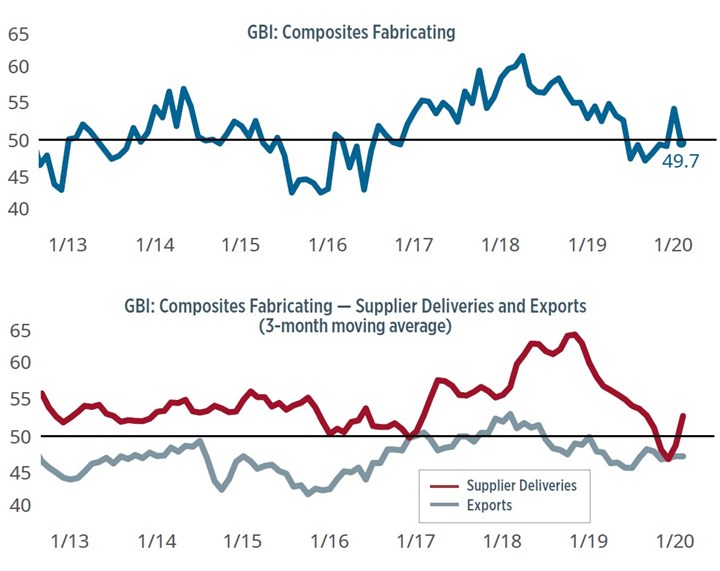

Composites Index contracts on weak backlogs

For February 2020, the Composites Index contracted slightly with a reading of 49.7.

.jpg;width=70;height=70;mode=crop;format=webp)

The Composites Index contracted slightly in February as backlog activity contracted amid a sharply slowing growth in production and new orders activity. Gardner Intelligence expects that most — if not all — of its indicators will be subjected to shocks from COVID-19. That the virus originated in Asia suggests that American manufacturers in the immediate future should pay particular attention to their supply chains and expect increased volatility in export orders and material prices.

After January’s expansionary reading — the first since mid-2019 — the Composites Index contracted slightly in February to register 49.7. Gardner Intelligence’s review of the underlying components observed that the Index in February reported little new expansionary activity in production and new orders after both registered recent highs the month prior. The fastest expanding component was supplier deliveries, while the Index was pulled lower by a sharp contraction in backlogs and a continuing contraction in export activity.

Manufacturing outlook as a result of COVID-19

The impact of COVID-19, widely known as the “Coronavirus,” is expected to have an adverse effect on the Composites Index in the coming months. The efforts of Asian governments in January and February — and by a widening collection of nations in February and March — to combat the spread of COVID-19 while necessary, is also having a detrimental impact on the world’s supply chain, as workers, companies and cities are affected by quarantine measures. This will most immediately restrict the normal flow of upstream and sub-component goods that are necessary for the proper functioning of the manufacturing sector.

The Composites Index is unique in its ability to meticulously measure business conditions specific to the composites industry on a monthly basis. This means that moving forward this Index will be able to quantify both the initial shock from the virus along with the timing and strength of the composites industry’s eventual recovery.

At this time, it is particularly important for our readers to complete the GBI survey sent to them each month. Your participation will enable the best and most accurate reporting of the true magnitude and duration of COVID-19. It will allow you and your peers to make data-driven decisions at a time when there may be a strong temptation to make impulsive decisions that could make a difficult situation worse.

Related Content

-

Longtime partner New Flyer selects Hexagon Purus to outfit hydrogen transit bus

Hexagon Purus will continue to supply Type IV hydrogen tanks for the Xcelsior Charge H2 fuel cell electric bus, the tanks of which will be produced out of Hexagon’s new Maryland facility.

-

Composite sidewall cover expands options for fire-safe rail components

R&D project by CG Rail explores use of carbon fiber-reinforced thermoplastics and recycled manufacturing scrap to meet fire safety, weight and volume targets.

-

New Flyer selects Hexagon Purus H2 tanks for fifth consecutive year

Type 4 tanks will continue to be supplied for the mass mobility provider’s Xcelsior Charge FC fuel cell electric transit buses.